You placed your final take profit at a level that made sense. A structural high, a measured target, a clean R-multiple. You had a reason for it.

Then the trade went your way. It moved, it built, it looked exactly like it was supposed to. And you closed the whole position. Not a partial — everything. You told yourself it was the right call, that locking in the gain was disciplined, that you were protecting the account.

Then you watched the trade carry on and hit your original target anyway.

This is not a discipline problem. It is not even really a psychology problem. It is a sizing problem, working in reverse.

The same issue as position sizing, wearing a different mask

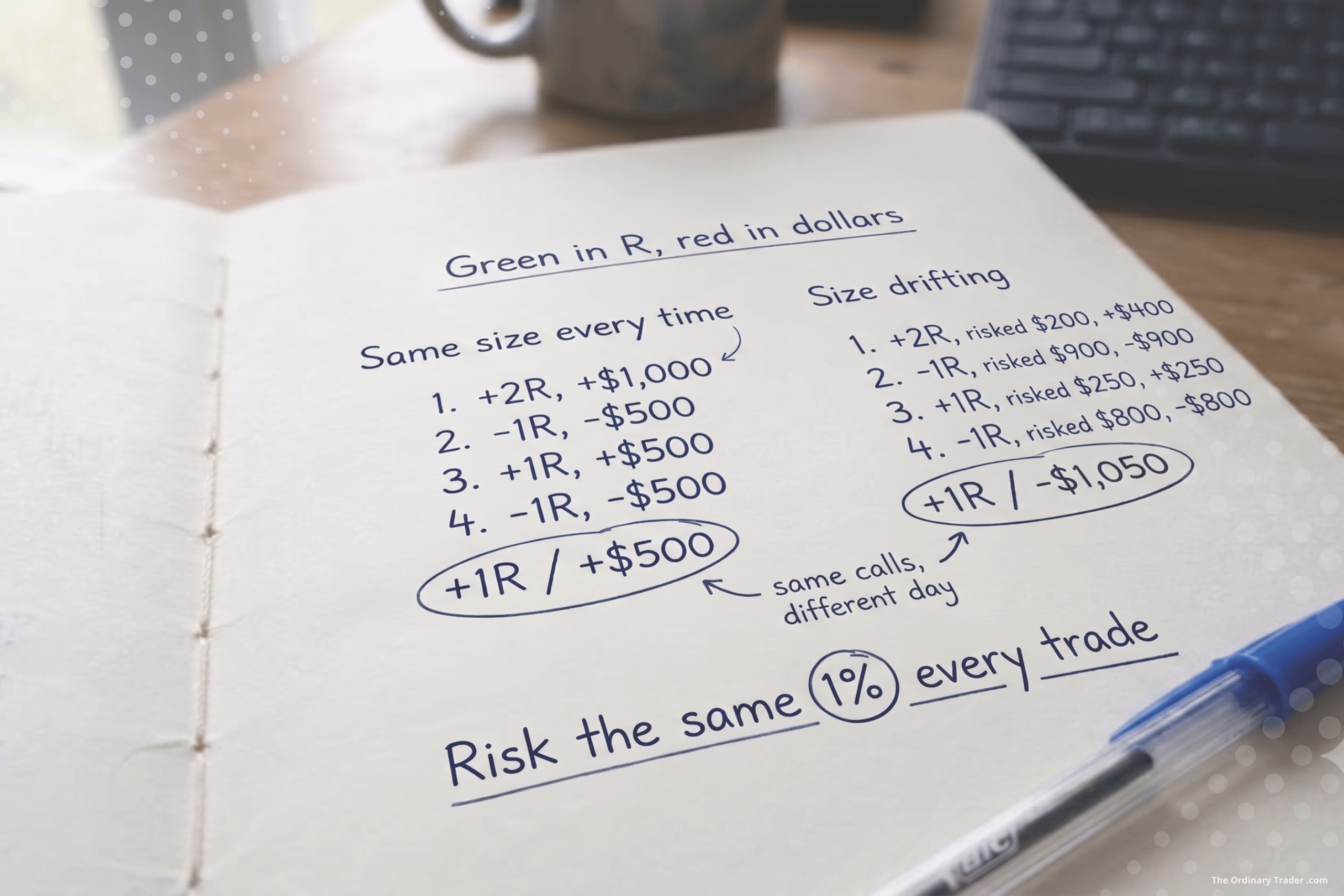

Last week’s post was about what happens when your position is too large going into a trade. The nerves. The inability to hold a stop calmly. The way a losing trade feels catastrophic when the size is wrong.

The same mechanic applies on the way up.

When your position is oversized, you do not just feel the losses more intensely. You feel the gains more intensely too. A trade that is running in your favour starts to show you a number in green that feels real and meaningful and, critically, fragile. The thought arrives quietly: what if it turns? What if I give all of this back?

So you close it all. You take the full profit early. And you call it sensible.

The trade did not fail. The size made it impossible to sit in.

When your position is oversized, you do not just feel the losses more intensely. You feel the gains more intensely too.

You do not fully trust where your TP is or why

The second reason traders close too early is that they placed a target at a level they do not really believe in.

If you understand market structure, your final TP is at a structural level for a reason. It is where the previous high sits, where liquidity will be drawn, where the market is likely to reach before it decides what to do next. You placed it there because the chart told you to.

But if you placed it there because it looked like a round number, or because someone else suggested it, or because it was “about right,” you will not trust it when the trade is mid-run. The doubt arrives the moment the price pauses or consolidates, and the easiest way to resolve doubt is to exit.

Understanding why your target is where it is makes it much easier to stay in the trade long enough to hit it. The structure holds the stop in place. It holds the target in place too.

Markets move in waves. Pullbacks are not reversals.

Price does not go from your entry to your final TP in a straight line. It pushes, pulls back, consolidates, and then continues. This is normal. It is how markets move.

But when you are watching a trade tick by tick, a pullback mid-run feels like the trade is breaking. You were up a meaningful amount. Now that number is smaller. The instinct is to protect what is left before it disappears entirely.

Most of the time, what you are watching is just the trade breathing. The structure is still intact. The original reason for the trade is still valid. The pullback is not an exit signal. It is the market doing what it always does before continuing.

Stepping away from the screen during a live trade is one of the most underrated skills in trading. The trader who is not watching every tick is usually the one who is still in the trade when the final TP hits.

The part that actually helps: partials and break even

Taking some profit off the table is not the same as closing the whole trade early.

If you have sized correctly and the trade is moving your way, taking a partial at an intermediate level changes the emotional equation. You have locked in something real. The remaining position is now smaller. And if you move your stop to break even at the same time, what is left cannot lose.

That combination – a partial taken at a reasonable point and a stop moved to entry – gives you a guaranteed outcome on the trade. You have already won something. What is left can run to the final TP without the same weight of anxiety sitting on it.

This is not the same as closing everything early. It is managing the trade in a way that lets you hold the rest of it calmly.

The pullback is not an exit signal. It is the market doing what it always does before continuing.

The calculation came before the emotions

Your final take profit was set before the trade opened. You looked at the chart with no position on, no money at risk, no emotional stake in the outcome. You found the level that made sense.

Then the trade opened, money went on the line, and the feelings arrived. The number in green started talking.

The decision to close everything early is made by someone who is inside the trade, watching every tick, feeling the weight of potential loss on a gain that has not yet been secured. The original TP was set by someone who was none of those things.

When those two decisions conflict, trust the one that was made from the outside.